Marshall School of Business, USC

Business Field Project

at

Health Net, Inc. Investment Department

Hedging the volatility of Claim Expenses using Weather Future

Contracts

by

co written by

Emin Gabrielyan, PhD

Table

of Contents

Influenza Like Illnesses (ILI) and

Temperature Correlation

ILI as a Function of Temperature

Price probability density

transformation

Neutral (right) price of Futures

Probability density function of

insured costs and futures with right prices

Finding the optimal strike price and

volume of futures

Overview

The

purpose of the paper is to identify the correlation between weather temperature

patterns and Health Net, Inc. operation expenses and propose cost hedging

strategy using weather future contracts. The strategy is meant to decrease the

volatility of Company’s claim expenses throughout the year.

Observation

of historical data indicates that flu related illnesses consistently start from

November and last until May of each year.

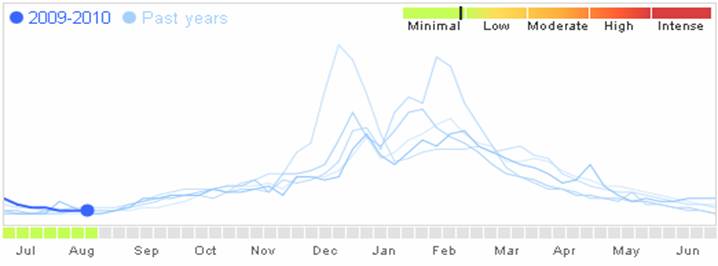

The following chart shows 2008 to 2009 flu trend in

![]()

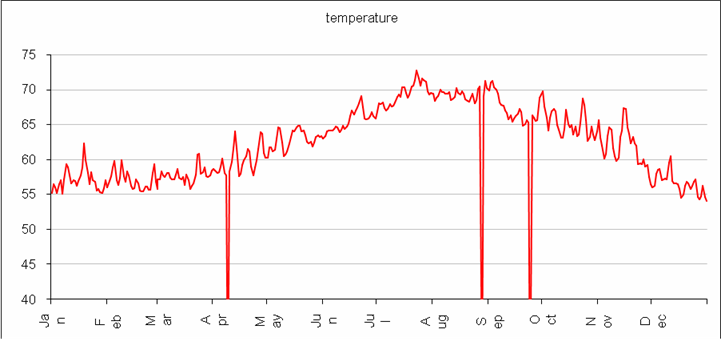

As you

can see the flu season picks during the coldest months of the year, December to

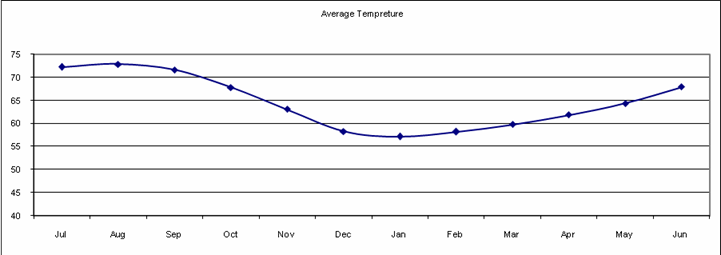

March. The following chart shows the daily average weather temperature trend in

![]()

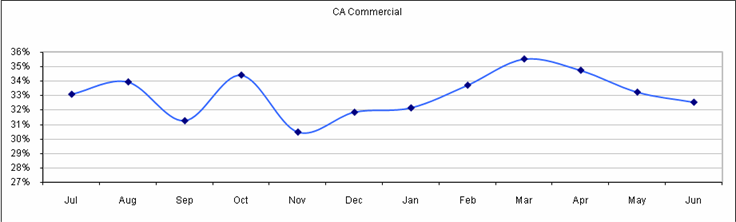

The table

bellow shows the number of Health Net’s provider claim receipts for

|

|

Jul-08 |

Aug-08 |

Sep-08 |

Oct-08 |

Nov-08 |

Dec-08 |

Jan-08 |

Feb-08 |

Mar-08 |

Apr-08 |

May-08 |

Jun-08 |

|

Receipts |

429,160 |

438,524 |

403,605 |

442,639 |

391,065 |

408,075 |

428,135 |

444,627 |

466,394 |

453,089 |

434,268 |

424,140 |

|

Membership |

1,296,915 |

1,292,110 |

1,290,667 |

1,286,349 |

1,282,481 |

1,281,007 |

1,331,490 |

1,318,908 |

1,313,263 |

1,304,342 |

1,306,500 |

1,303,301 |

|

Receipts per Member |

33.09% |

33.94% |

31.27% |

34.41% |

30.49% |

31.86% |

32.15% |

33.71% |

35.51% |

34.74% |

33.24% |

32.54% |

![]()

![]()

This

analysis indicates that the number of receipts per member picks not in January-February, the coldest

months of the year with the most flu related illnesses but in March. This

perfectly correlates to the assumption of increased operating costs for managed

health care companies during flu season. There is a lag time between a doctor

visit and a claim submitted to the health insurance company by a provider. This

lag time averages at a little above one month.

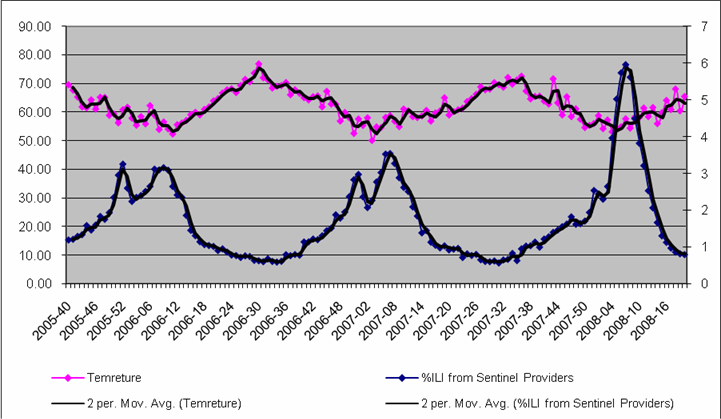

Influenza Like Illnesses (ILI ) and Temperature

Correlation

The regression analysis of

|

SUMMARY

OUTPUT |

|

|

|

|

|

|

|

|

|

Regression

Statistics |

|

|

|

|

|

|

|

|

|

Multiple

R |

0.6960837 |

|

|

|

|

|

|

|

|

|

0.4845325 |

|

|

|

|

|

|

|

|

Adjusted

|

0.4807142 |

|

|

|

|

|

|

|

|

Standard

Error |

0.7963725 |

|

|

|

|

|

|

|

|

Observations |

137 |

|

|

|

|

|

|

|

|

ANOVA |

|

|

|

|

|

|

|

|

|

|

df |

SS |

MS |

F |

Significance

F |

|

|

|

|

Regression |

1 |

80.479981 |

80.479981 |

126.89817 |

3.661E-21 |

|

|

|

|

Residual |

135 |

85.618237 |

0.6342092 |

|

|

|

|

|

|

Total |

136 |

166.09822 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Coefficients |

Standard

Error |

t

Stat |

P-value |

Lower

95% |

Upper

95% |

Lower

95.0% |

Upper

95.0% |

|

Intercept |

10.434298 |

0.7731665 |

13.495539 |

8.282E-27 |

8.9052135 |

11.963383 |

8.9052135 |

11.963383 |

|

|

-0.1398187 |

0.0124119 |

-11.264909 |

3.661E-21 |

-0.1643656 |

-0.1152718 |

-0.1643656 |

-0.1152718 |

![]()

HDD

Weather

Futures are traded in Chicago Mercantile Exchange (CME). The contracts are on

the daily cumulative Heating Degree Days (HDD) and Cooling Degree Days (CDD)

for a month observed at a weather station.

HDD=max

(0,65-A) and CDD=max (0,A-65)

Where: A

is the average of daily minimum and maximum temperatures. One Future contract

is on $100 times the cumulative HDD or CDD for one full month. The historical

temperature average provided in the Table 2 is measured in

|

1906-2008 averages in |

Jul |

Aug |

Sep |

Oct |

Nov |

Dec |

Jan |

Feb |

Mar |

Apr |

May |

Jun |

|

Average Max |

81.94 |

82.55 |

81.33 |

77.23 |

72.87 |

67.29 |

66.03 |

66.93 |

68.52 |

70.57 |

72.65 |

76.63 |

|

Average Min |

62.55 |

63.19 |

61.90 |

58.35 |

53.30 |

49.23 |

48.19 |

49.38 |

51.03 |

53.13 |

55.97 |

59.20 |

|

Average Temperature |

72.24 |

72.87 |

71.62 |

67.79 |

63.08 |

58.26 |

57.11 |

58.16 |

59.77 |

61.85 |

64.31 |

67.92 |

|

HDD |

0.40 |

0.00 |

2.90 |

34.00 |

108.80 |

226.30 |

259.60 |

216.90 |

188.90 |

132.00 |

75.30 |

19.00 |

|

CDD |

217.60 |

239.60 |

195.40 |

110.90 |

44.70 |

11.10 |

8.40 |

11.40 |

18.90 |

30.60 |

46.50 |

98.50 |

![]()

For

Example, if we purchased one HDD future contract for January at a strike price

of 200 and if the average temperature held our pay off would have been (259.60-200)*$100=$5,960.

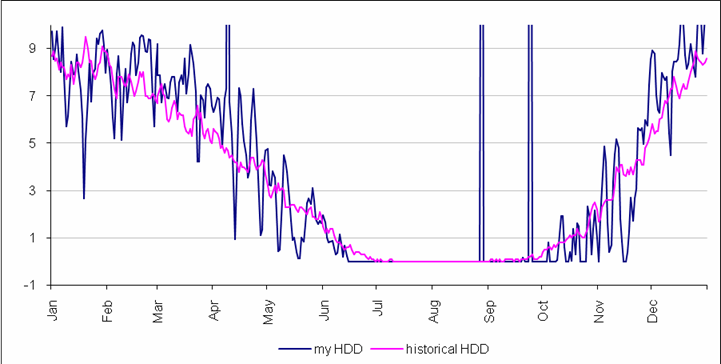

Historical average of daily HDD ranges from 0 to 9 and for month 0 to 270. However, HDD can reach as high as 750 in coldest parts of the world. Bellow is the temperature chart and a chart of deviation of my HDD calculation and WRCC HDD calculation based on historical daily average temperatures from1906 to 2008.

![]()

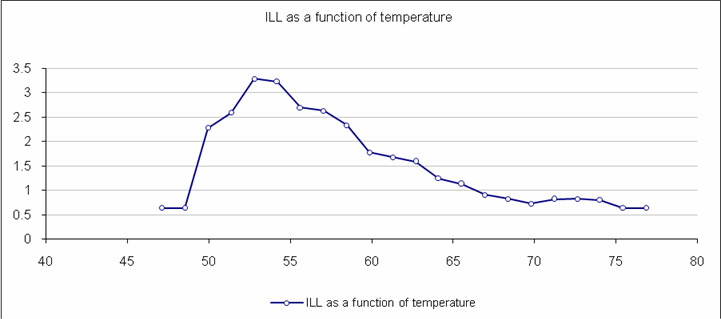

ILI

as a Function of Temperature

Incremental

percentage of

Similarly

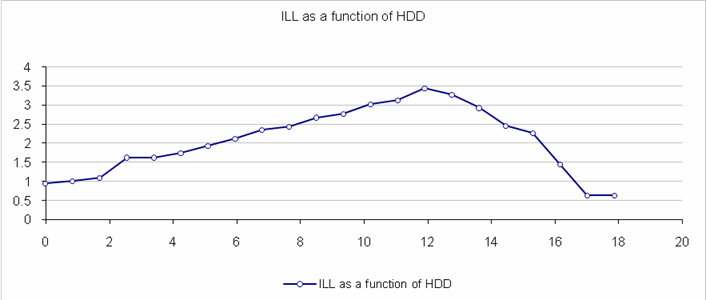

ILI incremental as a function of HDD is mirrored image of

Scaling Expenses to HDD

The purpose of the project is to hedge the flu season

Cost of Debt

Our

objective is to find futures' optimal strike price and volume to hedge the

enterprise expenses against volatility. For this purpose we introduce the

volatility cost of enterprise. On the other hand we shall introduce the profit

margin of the issuer of futures. In our model the average amount of

We

assume that the default debt cost (debtc) is equal to $300’000 (the

default price applicable for all scenarios where expenses end up at the average

of $12 mil). The multiplication factor (debtk) is a parameter changing

from 1.5 to 5. For instance if this factor is 2, it means that if the

enterprise ends up with an expense of $15.2 mil (i.e. one σ away

from the µ), it will cost extra $600’000 to the company (e.g. due to

short-term debt interests).

Price probability density transformation

In this section we analyze

transformations of a probability density of an operation cost, caused by

purchases of futures (issued on the same level of the cost). We assume two free

variables in the purchasing of futures, the strike price and the quantity of

futures. We assume that all futures are purchased with the same strike price.

When the operation cost exceeds the strike price, the futures cover the given

percentage of the operation cost excess.

That percentage depends on the amount of futures purchased. It can vary from 0%

to 100% (underinsurance) or can be more than 100% (over-insurance). The choice

of the quantity of purchased futures determines the insurance ratio.

The

probability density of the hedged price is computed as follows:

Where:

c is the cost of

purchased futures

a is the strike price

k is the insurance ratio

(1 corresponds to 100%)

Obviously:

The following animation shows how the probability curve of price changes

when the ratio of insurance changes from 10% to 250%. The strike price is the

same in all samples. The cost of futures is computed with a very simplified

empiric formula (it is sufficient for this demonstration). As expected, this

animation shows that the more you increase the insurance ratio toward 100%, the

narrower the volatility of your prices becomes. We also see that the price,

when over insured, never exceeds the strike price plus the cost of insurance.

Animation link:

http://switzernet.com/people/aram-gabrielyan/public/090817-hedging-cost-with-futures/

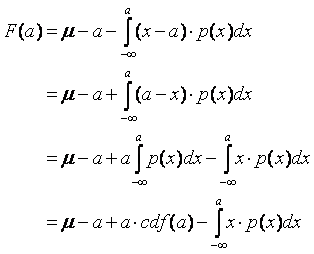

Neutral (right) price of Futures

Let

us have an operation price probability, a subject to normal Gaussian

distribution (see normal distribution):

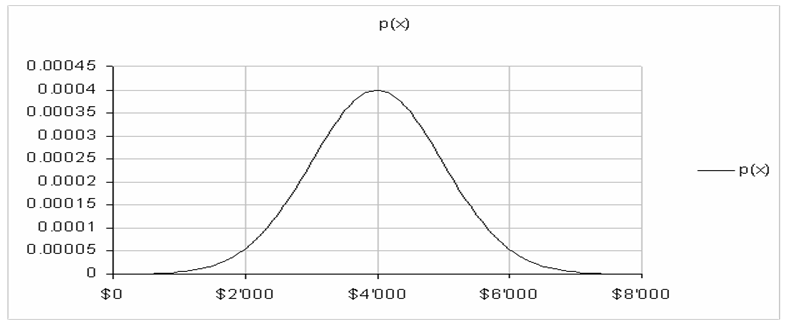

The

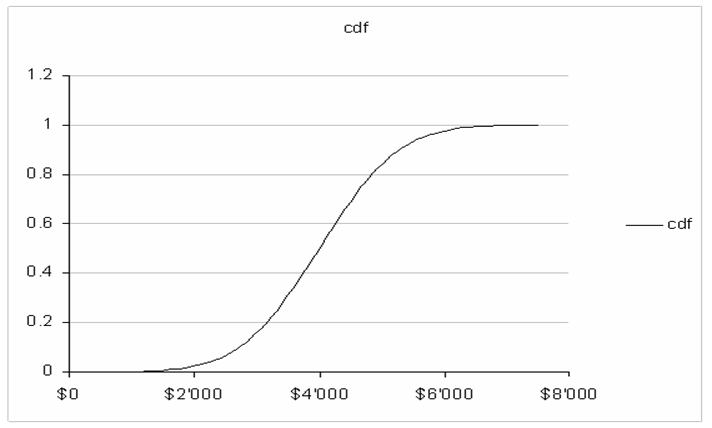

following chart shows such distribution, where the mean value is equal to

$4’000 and the variance is equal to $1’000:

We

seek to compute the ‘right’ price of futures (issued for our operation cost) as

a function of the strike price a. Such futures pay-off each additional

$1 of operation cost exceeding the selected strike price a.

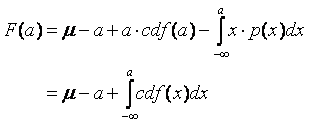

The

statistical ‘margin-less’ cost of such futures must be equal to:

The

cost computed in such a way contains neither a security nor a beneficiary

margin of the issuer of futures.

Using

the above formula the joined Excel file computes the cost of futures

straight-forwardly by summing refund claims weighted by their probabilities.

For each price exceeding the strike price, the formula takes the difference

between the price and the strike-price, multiplies it by the probability of the

price, and adds all of them together. The final sum is multiplied by the

distance between the sample points on the x axis.

Our

objective is to find the analytical formula of the price of futures (and if not

analytical then one using well known functions, such as the error function).

Due

to the symmetric bell shape of the normal distribution:

Therefore:

CDF

is the cumulative distribution function [see normal distribution].

It represents the probability that the price will fall below x (its

argument).

[xls]

[xls]

Considering

the product rule (see derivative):

![]()

We

can write that:

Therefore:

CDF

can be expressed via error function as follows (see normal distribution):

ERF

Excel function is implemented so no approximations or simulations is needed.

It is known that (see list of integrals):

Taking

into account the chain rule (see derivative):

The

CDF integral is computed as follows:

The

‘margin-less’ price of futures can be therefore expressed as follows:

The

following animation shows the price of futures as a function of the strike

price where the variance, i.e. the volatility, changes from $100 to $6500 over

the time. The mean value is always the same and is equal to $4000:

Animation link:

http://switzernet.com/people/aram-gabrielyan/public/090819-neutral-price-vs-Black-Scholes/

Probability density function of insured costs and futures

with right prices

In Price probability density transformation [090817 ii] we developed the probability density

function of operation costs insured by futures. This density is also a function

of selected strike price and of insurance ratio k (representing the pay-off

ratio of cost units exceeding the strike price a, or otherwise the amount of

purchased futures). In the document we assumed the cost of futures c as an input

parameter. No formula was provided for computing the cost of futures.

In

Neutral (right)

price of Futures [090819 ii] we developed a formula for computing the ‘right’ cost of

futures for a given strike price a. Under term ‘right’ or ‘neutral’ we

understand the price, such futures would cost to an insurance company taking

into account the volatility of the cost. This shall be an integral of excess of

operation prices exceeding the strike price a weighted by the normal

distribution of the operation price (see normal distribution).

The

formula of futures price that we developed in [090819 ii], is fully analytical, with the exception of error function

ERF implemented in Excel (see error function).

Because

the price of futures is right, if computed as follows:

![]()

The

following must hold for all a and k

In

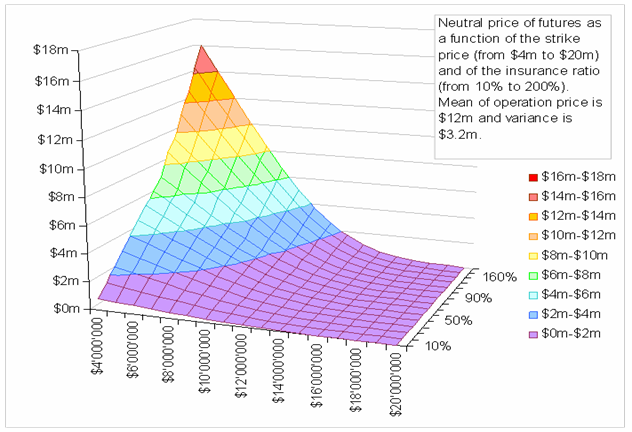

order to validate both of our formulas, we use an Excel model. The mean of our

operation cost at $12 mil and the variance is $3.2 mil. For a two-dimensional

set of parameters, (a) strike prices varying from $4 mil to $20 mil and (b) the

insurance ratios varying from 10% to 200%, we compute ‘right’ prices of futures

using our formula ![]() . The blow chart

shows this function for the two dimensional set of input parameters:

. The blow chart

shows this function for the two dimensional set of input parameters:

Sub-sequentially,

based on the right price, we compute probability density values with our

formula ![]() by loading

results into an array with prices ranging from $0 to $23’500’000.

by loading

results into an array with prices ranging from $0 to $23’500’000.

The

following animation shows that the choice of a and k can change

the shape of price distribution significantly:

Animation link:

http://switzernet.com/people/aram-gabrielyan/public/090819-average-of-hedged-cost/

By

having, for each shape (dictated by a pair of strike price a and

insurance ratio k) of the probability density array we compute the mean

of the insured operation cost:

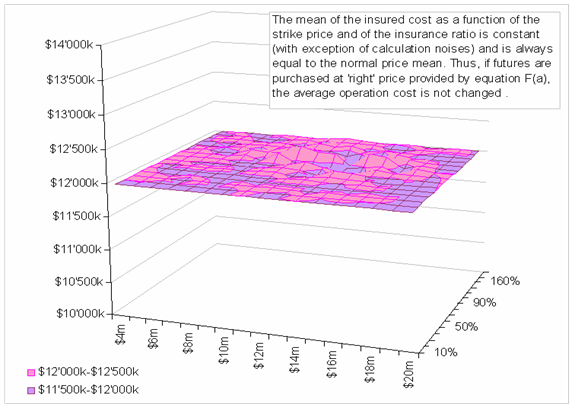

Irrespectively

how wildly the probability density shape is changed (by the choice of two

parameters of futures), the Excel simulation shows that the computed mean of

insured operation costs is always equal to the mean of the uninsured costs,

i.e. to µ (with exceptions of

precision errors). This suggests no hidden costs in prices of futures.

The

results of this simulation validate our two formulas for calculation of the

‘right’ price of futures ![]() and

subsequent calculation of the insured costs' probability density

and

subsequent calculation of the insured costs' probability density ![]() .

.

Finding the optimal strike price and volume of futures

In

our model we deal with future contracts that can pay-off a portion of

enterprise expenses exceeding a pre-selected strike price. The choice of the

pay-off portion (of the excess with respect to the strike price) is made by the

choice of the amount of purchased futures. This fraction can be less than, more

than, or equal to 1. This model is applicable to a more general case, where

instead of futures issued directly on the enterprise expenses, the futures are

issued on another underlying instrument highly correlated to the enterprise

expenses. HDD future contracts are a good example of such instruments.

Our

objective is to find the optimal strike price and volume of futures, purchased

for hedging the enterprise expenses against volatility (see Cost of Debt section.)

In

[090817 ii] we developed price probability density transformation

achieved by the purchase of futures. In [090819a ii] we developed a formula for computing the neutrally or

right price of futures. In [090819b ii] we showed that the mean of insured expenses does not

change, if the futures are bought at neutrally right prices. This means that if

the market price of futures is always right, we are definitely interested in

purchasing futures all the time, even if the volatility cost is low. Futures

are narrowing the probability density of expenses and are therefore minimizing

the volatility related debt costs.

However

the pleasure of having a future based insurance shall often have a market cost

exceeding its neutrally right price [090819a ii]. The difference between the market price of futures and

the right price computed by our formulas [090819a ii] is precisely the cost of this pleasure. This cost must be

counterbalanced with savings achieved on the volatility side. The margin added

on the right price of futures is represented in percentages. We analyze a range

from 0.5% to 90%.

In

the following chart we assume that the default debt cost (debtc) is

equal to $300’000 (the default price applicable for all scenarios where

expenses end up at the average of $12 mil). The multiplication factor (debtk)

is a parameter changing from 1.5 to 5. For instance if this factor is 2, it

means that if the enterprise ends up with an expense of $15.2 mil (i.e. one

variance away from the mean), it will cost extra $600’000 to the company (e.g.

due to short-term debt interests) (see Cost of Debt

section.)

The

surface shown in the animation below represents the overall cost (the

volatility debt cost together with the profit margins paid to issuers of

futures) as a function of the strike price (in the range from $4 mil to $20

mil) and the insurance ratio (in the range from 10% to 200%). The animation

shows the changes in the shape when changing the issuer's profit margin

(fairness) and the debt cost factor (dependence). For each frame (i.e. for each

pair of fairness of futures and dependence of enterprise from the volatility),

the text data panel shows the best recommended strike price and insurance

ratio.

This

animation demonstrates the concave shaped form of the surface for all pairs of

fairness and dependence showing that

there is always an optimal choice to make depending on the market prices of

futures and the extra cost of the volatility of the enterprise expenses.

Animation link:

http://switzernet.com/people/aram-gabrielyan/public/090820-best-strike/

Files and References

Hedging the volatility of Claim Expenses using Weather Future Contracts (this document):

http://switzernet.com/people/aram-gabrielyan/public/090823-hedging-with-weather-futures/

http://unappel.ch/people/aram-gabrielyan/public/090823-hedging-with-weather-futures/

This document in Web [htm], [doc] and printable formats [pdf], [doc], [docx]

Finding the optimal strike price and volume of futures for hedging against the volatility of enterprise expenses:

http://switzernet.com/people/aram-gabrielyan/public/090820-best-strike/

http://unappel.ch/people/aram-gabrielyan/public/090820-best-strike/

Validation of the formula of the ‘right’ price of futures and of the function of the insured price’s probability density:

http://switzernet.com/people/aram-gabrielyan/public/090819-average-of-hedged-cost/

http://unappel.ch/people/aram-gabrielyan/public/090819-average-of-hedged-cost/

Right price of futures as a function of the strike price:

http://switzernet.com/people/aram-gabrielyan/public/090819-neutral-price-vs-Black-Scholes/

http://unappel.ch/people/aram-gabrielyan/public/090819-neutral-price-vs-Black-Scholes/

Probability density of a hedged price:

http://unappel.ch/people/aram-gabrielyan/public/090817-hedging-cost-with-futures/

http://switzernet.com/people/aram-gabrielyan/public/090817-hedging-cost-with-futures/

* * *